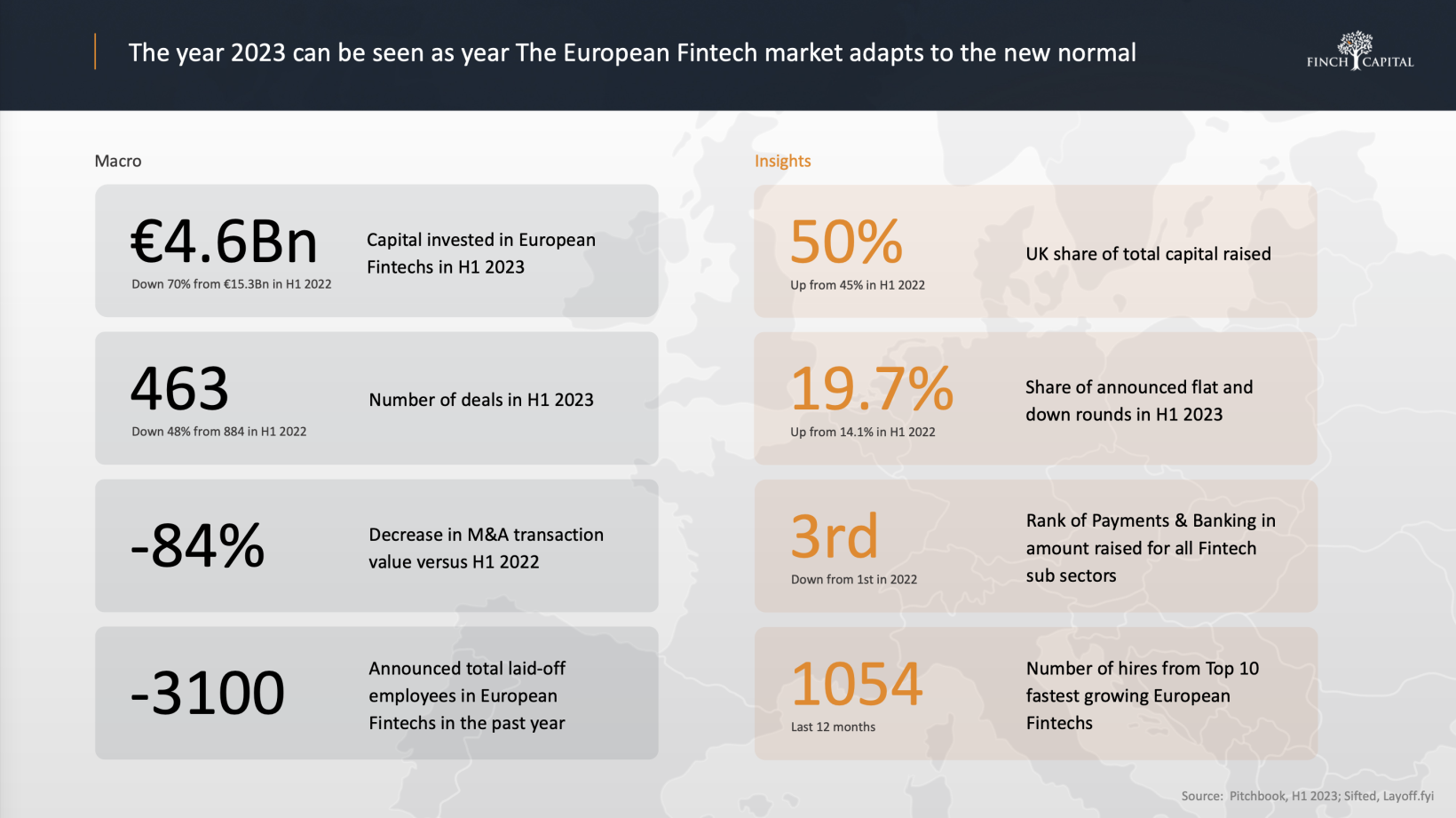

Fintech funding in Europe has been greatly affected by the challenging economic environment, the latest report by Finch Capital has found. Specifically, startups in the sector raised a total of €4.6bn in the first half of 2023 — down 70% from €15.3bn in H1 2022.

“Since mid-2022 we have seen an increase in investment discipline in public and private markets, resulting in less funding, lay-offs, less IPOs, flight to quality, and focus on capital efficiency,” said Radboud Vlaar, Managing Partner at Finch Capital.

Amid this increased funding discipline, this year’s first half has seen a 48% decline in the number of deals (434 in total) alongside an 84% decrease in M&A transaction sizes, compared to the equivalent 2022 levels. On the bright side, overall M&A activity fell only by 5% with volumes to match those of the past year.

Meanwhile, although the top 20 funding rounds are back to pre-2020 levels, investment dropped the most for the rest, which accounted for less than 40% of the total deal volume. Startups in the Series A to C stages have felt the heaviest impact. In contrast, seed rounds continued to attract funding.

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

From a valuation perspective, public markets have withdrawn to 2019 levels, after record growth in 2020-2021, but are showing signs of stabilisation. Private markets are also transitioning to 2019 valuation levels at a comparable but slower pace.

“We should also start to see a slow recovery of the IPO market in the next semester as valuations have started to slowly pick up and inflation is declining,” noted Vlaar.

Crypto on the rise

Crypto and Lending have attracted most of the investments, displacing Payments and Banking — a traditionally resilient category that saw record capital deployed in 2022. Notably, one in three fintech startups are now labelled as crypto/blockchain.

From B2C to B2B

The report has also found that the trend of the past years towards B2B fintech is here to stay. One reason why is the growing interest in regulation technology as payments and open banking are increasingly consolidating. Another is generative AI’s potential applications in retail banking and the insurance sector.

The UK leads in funding

A well-established fintech hotspot, the UK has shown more resilience and accounted for over 50% of the funding in Europe.

Nevertheless, the UK, Germany, and France also saw a 70% decline in funding value, but optimistically, exits continued consistently. Poland recorded the biggest drop at 89.9%. Overall, countries with an active Series A-B investor base, have seen valuations hold up with small increases in post-money valuations.

The “new normal”

“Consolidation and more competitive investment flows, combined with still significant levels of undeployed capital, will bring maturity to the fintech sector. This new normal level of activity demonstrates the refocus of the fintech ecosystem on long term sustainability versus short term gains,” said Vlaar.

And although the overall environment will continue to be challenging in the next 12 months, he added that this will result in “a more healthy and sustainable startup, hiring, and investor ecosystem.”